Retirement Tax Planning for High-Income Earners

You built the income. Now build the structure that keeps it. Retirement tax planning for high-income earners is about designing how wealth survives the transition, not just filing accurately on the way out.

Complex Situations Only

Not every high earner has the same retirement problem. The physician in their peak earning years faces a different sequencing challenge than the executive with deferred compensation vesting across three tax years, or the real estate operator whose depreciation strategy needs to coordinate with retirement distributions.

We work specifically with:

If your tax situation involves more than one of these, the complexity compounds. So does the cost of getting it wrong.

At your income level, retirement planning is a structural decision, not a savings habit. These are the four strategies that determine how much of what you've earned actually makes it through retirement intact.

Roth Conversion Strategy

The conversion decision spans multiple years. We identify the lowest-bracket windows in your income trajectory and convert deliberately, shifting assets into a tax-free position before RMDs begin.

Retirement Entity Coordination

Your entity type controls which retirement vehicles are available and how much you can contribute. We match the right vehicle, Solo 401(k), SEP IRA, or defined benefit plan to your structure before income is earned.

RMD Distribution Planning

Unmanaged RMDs stack on top of Social Security and investment income, often at peak bracket rates. Sequencing starts years before distributions are required, not the year they arrive.

Social Security Timing

Claiming age, bonus elections, and NQDC plan decisions all interact. We coordinate them together because each one affects the taxability and timing of the others.

These strategies work best when built together. Handled in isolation, each one leaves money on the table.

Before you hire, expand, restructure, or reprice, KB Tax Devisers gives you the financial analysis to move with confidence. Here are the questions we answer every day.

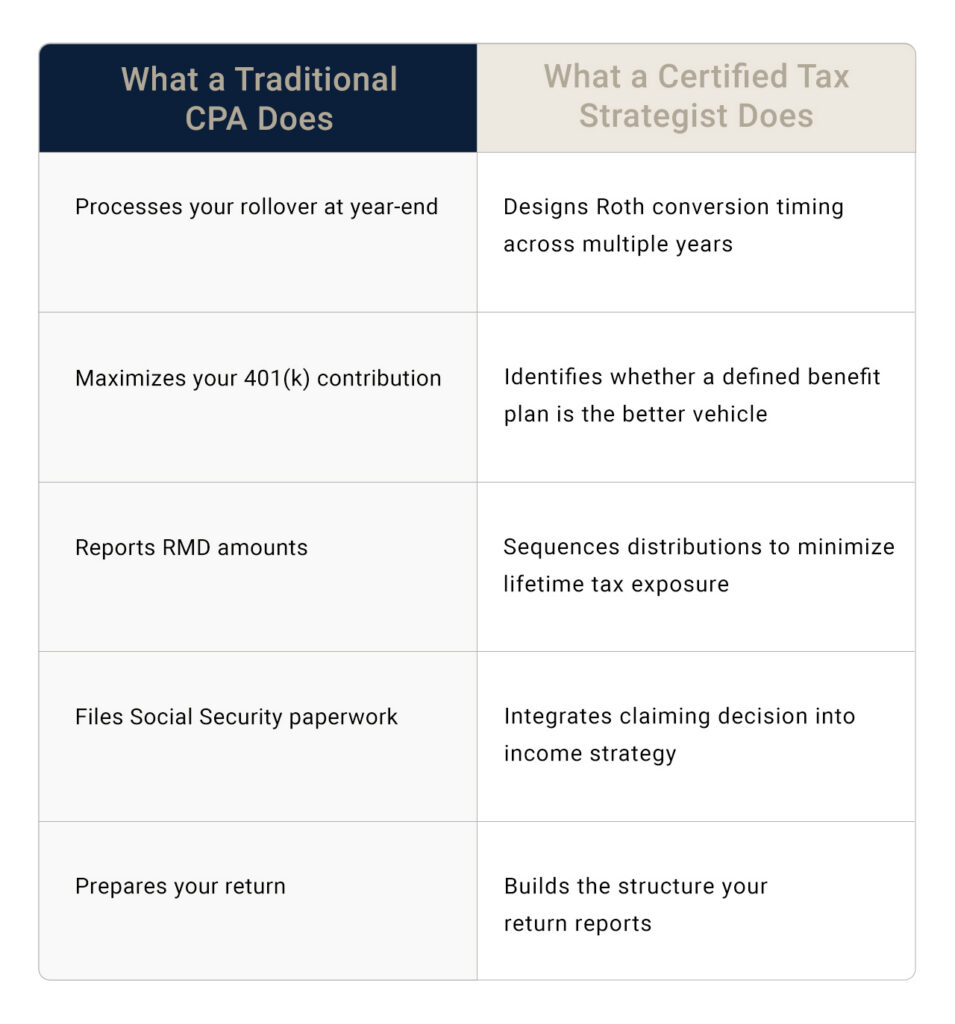

What a Traditional CPA Does

Processes your rollover at year-end

Maximizes your 401(k) contribution

Reports RMD amounts

Files Social Security paperwork

Prepares your return

What a Certified Tax Strategist Does

Designs Roth conversion timing across multiple years

Identifies whether a defined benefit plan is the better vehicle

Sequences distributions to minimize lifetime tax exposure

Integrates claiming decision into income strategy

Builds the structure your return reports

We diagnose before we prescribe. Every engagement begins with a complete review: three years of business and personal returns, current entity structure, all income streams, and your goals for the next decade and beyond.

Full picture review

We look at everything at once, entities, accounts, compensation, and personal financials, because the gaps are almost never isolated to one area.

Gap identification

Every structural inefficiency is quantified in dollars. Not estimated. You see exactly what your current setup has been costing you, year by year.

Written strategy

A documented, IRS-cited plan that coordinates your retirement vehicles, income structure, entities, and investment activity as one system.

Quarterly oversight

Tax law changes. Your income changes. Your strategy adjusts accordingly before the impact lands on your return.

It's the proactive design of how income flows through entities, accounts, and investments to minimize tax exposure before and during retirement, not just at filing time.

As early as possible. The most valuable planning windows open a decade or more before retirement, when Roth conversions, entity restructuring, and contribution strategies still have time to compound.

Your entity type determines which retirement vehicles are available. S-corp owners, sole proprietors, and partners each face different contribution limits and options, including solo 401(k)s, SEP IRAs, and defined benefit plans.

A Roth conversion moves pre-tax retirement assets into a tax-free account. High earners benefit most during low-income years or before RMDs begin; converting in stages reduces lifetime tax exposure.

A defined benefit plan funds a target retirement benefit, allowing contributions that far exceed standard 401(k) limits. It suits high-income earners with shorter accumulation windows who need to shelter more income now.

RMDs are taxed as ordinary income and stack on top of Social Security and investment income. Without sequencing, they can push retirees into high brackets at the exact point when income flexibility is lowest.

The optimal claiming age depends on your other income sources, since up to 85% of Social Security can be taxable. Coordinating the claim with a Roth conversion strategy in progress often produces the best combined outcome.

Yes, when structured intentionally. Depreciation from rental properties offsets taxable income annually. At retirement, coordinating depreciation recapture timing with distribution sequencing can meaningfully reduce the overall tax burden.

A certified tax strategist designs your tax structure before income is earned. A traditional CPA reports what already happened. There are only 55 Certified Tax Strategists in the United States.

If your CPA reviews your situation once a year at filing time, gaps almost certainly exist. A full diagnostic, covering three years of returns, entity structure, and income streams, identifies exactly what your current setup is costing you.

A single structural gap, the wrong entity type, an uncoordinated Roth conversion, or RMDs that weren't sequenced can cost a high-income earner hundreds of thousands over the course of a retirement. The earlier the review, the more options remain available.